Your organization’s insurance documents hold quite a bit of information, and they are not always the easiest to understand. In this blog, we are going to summarize a specific section of those pages: the coverage limit of your building and the contents.

Under each building listed on the insurance documents, there will be two “limits of coverage”, one will be for your building and the other for your organization’s personal property.

Building Limit

The building limit represents the amount of coverage that would be provided to replace the building in the event of a loss. Some example losses include: a fire, tornado damage, or hail damage. The cost to replace an existing building is often more expensive than an entirely new build because demolition and clean-up of the old building.

When reviewing the building coverage limit, one questions we’re often asked, “Why is the amount so much higher than what we can sell it for?” The reason being we are not covering for how much it would be to purchase, but instead looking at the cost of replacing the building. This limit will include costs for materials, labor from contractors, as well as demolition charges if necessary.

When to Review Your Building Limit

Here are three examples when we will review the coverage limit for the building:

- Every renewal of your insurance policy, your building limit will be reviewed. As prices of goods and services increase, it is essential that coverage for your building is increased as well to protect you against being underinsured.

- If any building renovation projects are being completed. For example, if your organization were to add a new section to your building, we would increase the building limit to include coverage for the addition.

- Rather than paying for coverage of unused building sections, you could save money by removing that section from your policy. For example, if your church building has empty classrooms that you never plan to use again, you can remove that section from your policy coverage.

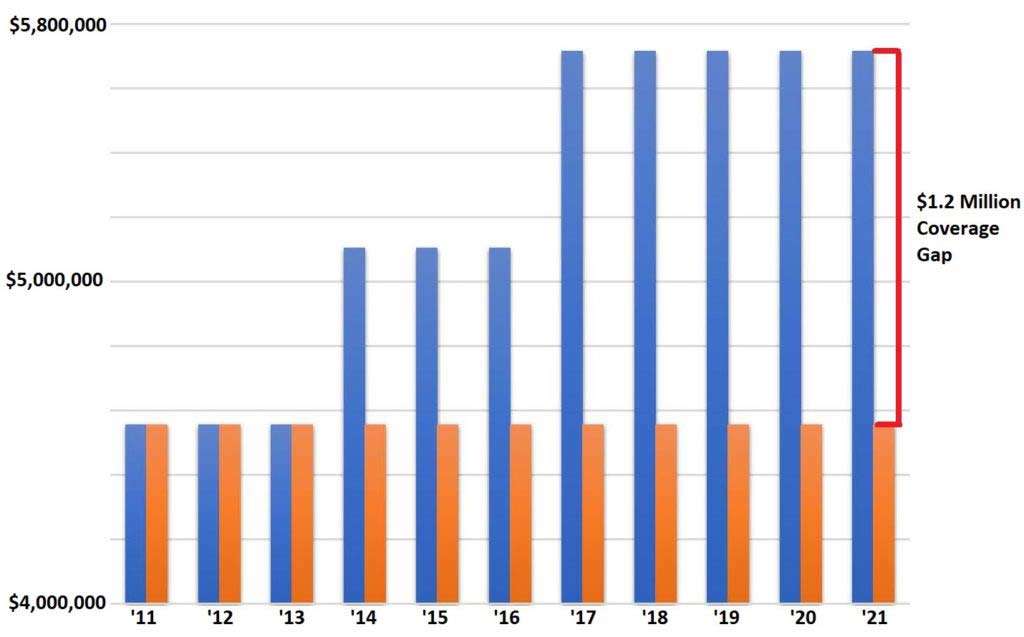

Let’s say your building limit was $4.5 million in 2011. Building limits increase on average 4% annually. In 2021, that would make your limit $5.7 million, assuming you accepted the increase at each policy renewal. If you opted to maintain the $4.5 million limit, you would have a gap in coverage of approximately $1.2 million.

This amount might seem excessive, but you have to take into consideration the costs of construction, costs of labor, update construction ordinances and code, and a slew of other factors. For example, the 2020 COVID-19 pandemic has created a shortage of lumber and building materials, driving lumber costs up 188% or more.

How to Calculate Building Coverage Limit

Now, you may ask how is the building limit determined?

We will ask specific questions regarding your organization’s property that will help determine the limit like:

- Square footage

- Construction Type

- Number of Stories

- Age of Building

- Roof Type

Using these details, we can calculate your building replacement cost and coverage limit.

And while this method of calculating the building limit is quite accurate, we still suggest having your property appraised by an industrial appraisal specialist every 7-10 years.

This will not only help you understand the replacement cost of your property, but it will also help you understand the market value of your property, in case your organization ever decides to sell your building.

Personal Property Limit

The personal property limit represents the amount of coverage that would be provided if there was a loss and we needed to replace the property in the building. To determine the right amount of coverage, we will ask for the value of your personal property. If you do know the values, here are a few ways to consider:

- Create an inventory of your organization’s property, and continually update it. We suggest organizing the inventory list by type of item, or creating an inventory by room. Be sure to keep a copy with your insurance agent.

- With higher value specialized property, fine art, stained glass, special technology; we can list those items specifically to ensure they are properly protected.

- If you do not know the value of your personal property, we recommend 18-20% of your building limit. For our clients, we have found that percentage range to be most accurate when calculating personal property value.

The Different Kinds of Valuations

When discussing your organization’s building and personal property limits, it’s also important to discuss what their valuation type is. On your declaration pages next to the building or personal property limit, you’ll see a spot showing “valuation type”, and you’ll see one of the following options:

- Replacement Cost

- Actual Cash Value

- Market Value

Replacement Cost

The Replacement Cost valuation insures your property for what it would cost to repair or replace your damaged property. It is the most common type of valuation as it provides the highest level of coverage.

Actual Cash Value

Actual Cash Value is calculated by subtracting depreciation from replacement cost and that will be your coverage limit.

For example, you buy a brand new laptop for $1,000 and it has a usable life of four years. Lets say two years later, that laptop is stolen and you have to replace it. Your insurance policy will only pay $500 for that laptop because of depreciation.

The laptop depreciates in value $250 per year. After two years it will have a cash value of $500. This is an example of Actual Cash Value.

Market Value

Market Value refers to how much you could sell your property for on the market. This provides the least amount of coverage, as this value is focused on what you could sell the building or contents for, not the amount you would need to replace the building or contents.

Review Your Building & Personal Property Limits

Not having accurate building and personal property limits can put your organization at risk. However, that is exactly why we review those limits with our clients once a year and ask that you contact us with any new building construction projects, new equipment, or personal property purchases.